Sustaining income after a divorce

Jane is 50, has two children, aged 17 and 18, and is in the middle of a divorce. She wanted to understand what the initial proposal for the separation of marital assets would mean for her: whether she could maintain her current standard of living, and also help her children financially when they are older.

Jane is also keen to continue to receive an income in line with her current annual expenditure of £60,000. Her income is primarily from buy-to-let properties, and it is important to factor in both the tax liability on this income and the impact of inflation throughout her retirement.

Given that Jane is not familiar with managing her finances, and is also on long-term sick leave from her civil service job, her lawyer introduced her to Nedbank Private Wealth. She believed in selecting a wealth manager that could manage all of Jane’s finances going forward on her behalf. As a bank, we can help with borrowing, as well as investments and wealth planning. We used cashflow modelling to help visualise Jane’s financial future and, importantly, to determine whether her wealth objectives could be met.

The planning process

The first step was to develop a full understanding of Jane’s financial position based on the proposed divorce settlement, and to understand her short, medium and long-term goals and objectives. In addition, Nedbank Private Wealth was introduced to the husband, Ben, to similarly help him plan his own finances after the divorce was finalised.

We developed a complete picture of their finances by assessing their current and projected wealth, along with their income and expenditure. We worked closely with their tax adviser to ensure they fully understood the impact of capital gains tax (CGT) on the transfer of marital assets after the divorce was final. The most significant tax consideration, in the context of separation or divorce, is likely to be a potential CGT liability when assets are sold or transferred from one spouse to the other as part of a financial settlement.

For many couples, the marital home is likely to be the most valuable asset to be considered in a divorce. Pensions are also a financial asset in scope, but are often the least understood and one of most complex assets to manage to facilitate a fair financial split. And given there is no legal obligation for these to be included in divorce discussions, there is little, if any, agreement on how the pensions should be valued or used to offset other assets. However, other assets and investments, including second homes, may also be significant in deciding any financial settlement.

Timing is key here.

However, if such a transfer takes place in a tax year after the couple has formally separated, assets will be treated as passing at market value and, accordingly, any gain in value since acquisition will be taxable on the transferring spouse, subject to any available relief.

As a client was going through a divorce, we helped her visualise her future finances to provide reassurance she could maintain her current standard of living and help her children financially when they are older.

The results

The use of cashflow planning helped us to develop a comprehensive financial plan that would enable Jane to understand what the proposed divorce settlement would mean for her and her children. In addition, it provided the reassurance that she would be able to manage her expenditure and allow her to make informed decisions with regard to both investments and estate planning. Finally, the plan was able to show Jane that she could afford to assist her children in buying their first homes, which was very important to her.

The ‘clean break’ divorce settlement involved Ben transferring his personal pension in full to Jane. This would help fund her expenditure in retirement, along with a final salary pension from her employment with the civil service. Jane will also request a forecast in respect of her state pension entitlement. Her personal cashflow plan also helped to identify the most tax-efficient strategy for the drawdown of her assets to meet her expenditure needs

We were also able to show her a number of different scenarios with regard to the buy-to-let property portfolio, should she wish to consider selling some of the properties in the future.

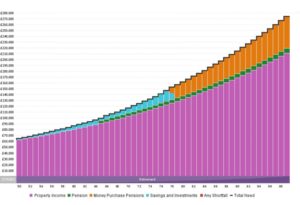

Last, but not least, Jane was reassured that the split of the assets would enable her to maintain her current lifestyle and not have to worry about going back to work (given her ill health), as the cashflow chart was not showing any red (indicating a shortfall between income needs and that which the financial assets could yield).

With the plan in place, we schedule a date for 12 months’ time given it is important that it is reviewed each year to take into account any lifestyle changes, and to ensure Jane remains on track to achieve her objectives.

In 2021, we held a series of three webinars focusing on divorce. These were: Managing your finances around a divorce; Divorce: beyond the financial and legal ramifications; and Divorce, pre-nups and pandemics – recent changes and those coming soon.

You can catch up on all of these demand on this website via the provided links. Please note that following the recording of these webinars the introduction of the 2020 Divorce Bill was postponed to April 2022.

Related news

You may also be interested in the following Insights

Contact

Get in touch to find out how we can help you with your financial challenges.

Clients of Nedbank Private Wealth can get in touch with their Wealth Adviser directly to understand how wealth planning can help them achieve their financial goals and objectives, or call +44 (0)1624 645000 to speak to our client services team.

If you would like to find out more about how we can help you with wealth planning support, please contact us on the same number as above, or complete the contact us form using the link below.

Any examples of investments and structures used are for illustrative purposes only. This webinar does not constitute an invitation or inducement to buy any financial investment or service. None of the content constitutes advice or a personal recommendation. Individuals should seek professional advice, based on their jurisdiction and personal circumstances, before making any financial decision.

Related case studies

Read about more clients we have helped

We have helped countless high-net-worth clients with their financial needs – some straightforward, some complex. Our bespoke approach, where we really get to know our clients, allows us to offer solutions that other wealth planners and private banks aren’t able to.

Thinking bigger: Unlocking retirement dreams

The opportunity to ‘think big’

Finding stability and confidence during divorce

Set for retirement

Start planning early